Options are used by investors to take advantage of a wide range of projections on the state of the market.

Unlike stock investing, where only a rise makes money, options can profit from falls in the market, and a range of other market movements such as changes in a security’s volatility.

One such simple strategy used in the long put, detailed here.

Description of the Long Put Strategy

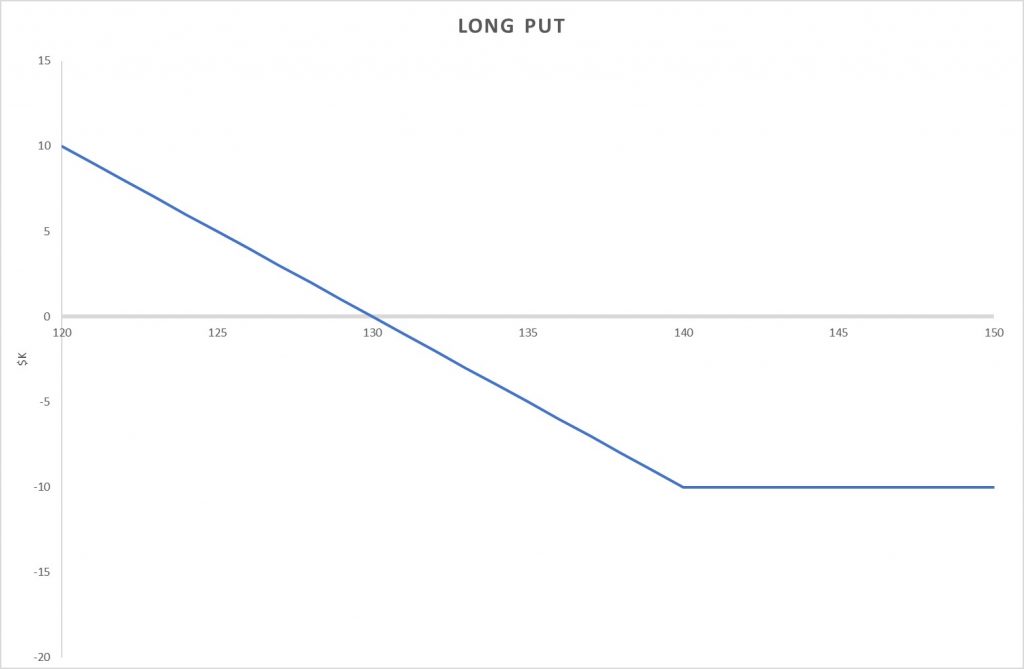

Long Put P&L Diagram

The strategy involves the purchase of a put option.

Puts give the buyer the right but not the obligation to sell the underlying security anytime* between now and the expiry date of the option.

This is for ‘American’ style options – as compared to European options which can only be exercised on the expiry date, not before. Most options traded on the CBOE that we’ll cover are American options.

For example suppose a put option was purchased with a strike price of 140 and 3 months of time remaining until expiry. Anytime over the next 3 months we could exercise the option and sell stock for $140/share.

(If we didn’t own stock we could buy some immediately before exercising the option – brokers would just pay the difference to us).

Maximum Gain and Loss of the Long Put

The maximum gain is significant, but is theoretically limited to the strike price minus the cost of the option, if the stock drops to $0.

Your maximum loss is the amount paid for the option. If the stock is anywhere above strike A, you will lose the same amount of money.

When and how to put a Long Put on

A long put would be placed if we believed the underlying stock was to fall, and fall quite rapidly (as we will see the put loses time value).

A long put position is initiated when a buyer purchases a put option contract. Puts are listed in an option chain and provide relevant information for every strike price and expiration available, including the bid-ask price. The cost to enter the trade is called the premium. Market participants consider multiple factors to assess the value of an option’s premium, including the strike price relative to the stock price, time until expiration, and volatility.

Typically, put options are more expensive than their call option counterparts. This pricing skew exists because investors are willing to pay a higher premium to protect against downside risk when hedging positions.

Long Put market outlook

A long put is purchased when the buyer believes the price of the underlying asset will decline by at least the cost of the premium on or before the expiration date. Further out-of-the-money strike prices will be less expensive but have a lower probability of success. The further out-of-the-money the strike price, the more bearish the sentiment for the outlook of the underlying asset.

Pros of Long Put Strategy

Long puts are a capital efficient position – only the cost of the option which is likely to be a fraction of the price of the stock is required.

They are also one of the few ways retail investors can profit from falls in stock prices. The alternatives such as shorting a stock are often unavailable or too capital intensive to non wholesale broker clients.

The position is also pretty simple compared to other strategies and options spreads we cover.

Cons of Long Put Strategy

Long puts are theta positive. Over time they lose value, all things being equal, and so any move down needs to be reasonably rapid to counteract this.

Care with the strategy needs to be taken if the stock has taken a large fall recently. out of the money puts in particular are likely to be in demand, push up implied volatility and option price.

Should the stock rise back in value the puts will likely lose twofold: from the negative delta of the position and also the implied volatility falling back to normal levels. The put price is likely to collapse in this scenario.

Risk Management

As we’ve stated above, ensuring a long put position doesn’t have an elevated implied volatility on entry is the first risk management decision to make.

You should also consider reasonably long dated options – 30-90 days plus – to minimize the loss of time value. Theta on longer dated options is lower hence minimizing the effect of time decay.

Another alternative is to sell an out of the money put to reduce the net cost of the strategy, and minimize time decay risk. This would turn the strategy into a bear put spread.

Long Put Strategy vs. Shorting Stock

A long put may be a favorable strategy for bearish investors, rather than shorting shares. A short stock position theoretically has unlimited risk since the stock price has no capped upside. A short stock position also has limited profit potential, since a stock cannot fall below $0 per share. A long put option is similar to a short stock position because the profit potentials are limited. A put option will only increase in value up to the underlying stock reaching zero. The benefit of the put option is that risk is limited to the premium paid for the option.

The drawback to the put option is that the price of the underlying must fall before the expiration date of the option, otherwise, the amount paid for the option is lost.

To profit from a short stock trade a trader sells a stock at a certain price hoping to be able to buy it back at a lower price. Put options are similar in that if the underlying stock falls then the put option will increase in value and can be sold for a profit. If the option is exercised, it will put the trader short in the underlying stock, and the trader will then need to buy the underlying stock to realize the profit from the trade.

Time decay impact on a Long Put

Time remaining until expiration and implied volatility make up an option’s extrinsic value and impact the premium price. All else being equal, options contracts with more time until expiration will have higher prices because there is more time for the underlying asset to experience price movement. As time until expiration decreases, the option price goes down. Therefore, time decay, ortheta, works against options buyers.

Implied volatility impact on a Long Put

Implied volatilityreflects the possibility of future price movements. Higher implied volatility results in higher priced options because there is an expectation the price may move more than expected in the future. As implied volatility decreases, the option price goes down. Options buyers benefit when implied volatility increases before expiration.

Conclusion

A long put is a position when somebody buys a put option. It is in and of itself, however, a bearish position in the market.

Investors go long put options if they think a security’s price will fall.

Investors may go long put options to speculate on price drops or to hedge a portfolio against downside losses.

Downside risk is thus limited using a long put options strategy.

The Long Put strategy is great for being able to simply and easily profit on the fall of an underlying security. However more sophisticated traders may be more attracted to more complex strategies such as the bear call spread to similarly profit, but as reduced cost and theta risk.

Related articles

Options Greeks: Theta, Gamma, Delta, Vega And Rho

Options Vega Explained: Price Sensitivity To Volatility

Options Theta Explained: Price Sensitivity To Time

Enter Your Information Below To Receive Trading Ideas and Latest News

Your information is secure and your privacy is protected. By opting in you agree to receive emails from us. Remember that you can opt-out any time, we hate spam too!